McV Compounding Founder Fund Strategy

McVinney Capital’s approach is built on a two‑layer systematic architecture — a long‑term compounding engine supported by a tactical short‑term layer. The system is engineered to capture structured spreads with bounded risk, reinforced by a disciplined process that recycles capital, reduces cost basis, and compounds over full campaign cycles.

This is not a reactive trading strategy. It is a mechanically defined system of systems designed to operate consistently across market regimes.

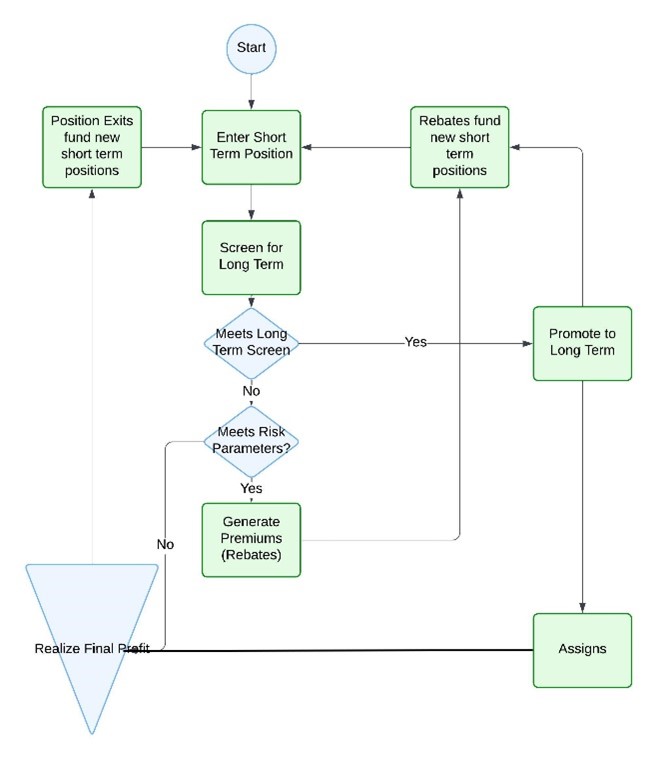

Figure 1: Systemic flow between short‑term and long‑term components.

The system begins with tactical short‑term positions that generate cash flow and screen for momentum. Qualified positions promote to long‑term compounding; all flows are governed by predefined rules.

What Makes the Strategy Different

- Structural Arbitrage — Initial entries exploit predictable mispricing between paired option legs created by platform valuation mechanics, market‑maker hedging behavior, and retail‑driven order flow. This generates short-term realized gains, reduces net cost basis, and improves long‑term economics.

- Promotion Logic — Positions advance from short‑term to long‑term only when structural alignment and sustained momentum are confirmed. This creates a disciplined pathway from cash‑flow generation to long‑term compounding.

- Bounded‑Risk Architecture — Both layers operate within predefined risk tolerances. Exits are engineered, not discretionary, and long‑term positions are structured to cap risk while preserving elevated upside capture.

- Capital Recycling — Realized short‑term gains and long‑term premium rebates continuously fund new entries reinforcing the compounding cycle.

How the Two Layers Work

Short‑Term Component

The short-term system is a tactical overlay that generates cash flow, screens for durable momentum, and reduces capital exposure. It captures structural arbitrage spreads that provide realized gains and improve long-term entry economics.

Long‑Term Component

A structured compounding engine built on deep‑in‑the‑money LEAP‑based positions. These positions capture engineered spreads with elevated upside caps, generate premium rebates, and convert short‑term gains into long‑term tax treatment.

Together, the two layers form a closed‑loop system:

rebates → fund short‑term overlays → screen and compound → promote or exit.

Risk & Discipline

The system is governed by predefined thresholds for promotion, continuation, and exit. NAV volatility reflects mark‑to‑market accounting — not realized economic outcomes. Value is realized through assignment or engineered closure, not daily price movement.

This is a campaign‑grade structure. Hold the system. Let time deliver. Exit only when the math demands it.